Glass Houses

Many of our clients who are older than 59 ½ are worried about a sudden and sustained collapse of the equity and bond markets. Those who aren’t should be. Yet they remain fully invested “in the market” because they need the yield on their money, and the banks offer only negative real rates of return after taxes and inflation. These folks stay in the market at their peril because they face massive downside market risk…a risk they really can’t afford to take. This is a perfect client profile for an Indexed Annuity solution.

Just as people who live in glass houses shouldn’t throw stones, people who are in or near retirement shouldn’t have massive market positions because they can’t bear the consequences of a 2008 style meltdown. They need to do things that make sense no matter what.

In this situation, Indexed Annuities make sense no matter what.

Over the past 15 years or so, the Dow has grown from 6500 (03-09-09) its post-crash low to an incredible 33470 (10-06-23). Now, one must keep in mind that one US Dollar in 2009 would now be worth $1.43 in 2023 dollars due to inflation. Or to put it another way, it now takes $1.43 to buy what would have taken only $1.00 in 2009. Nonetheless, whether we accept the nominal increase, or an inflation adjusted increase, that is one phenomenal increase. But it was all engineered and not the result of genuine market forces.

How does this happen?

Here are some ways the Federal reserve intervenes in what is supposed to be a "free capital market” system.

1. The FED can buy or sell more debt (bonds) and thereby increase of decrease bond yields at will.

2. The FED can buy or sell stocks thereby directly manipulating the Dow.

3. The FED can and does support the equity markets by increasing the money supply thereby creating asset price inflation.

This shows up as ever higher account “values” in retirement accounts. As one broker I knew said, “people don’t care how it happens or what it means, all they care about is seeing higher numbers on their statements.” Hmmm.

People tend to have short memories. We at Slingshot Capital do not. In 2009, we had clients in Variable (market based) Annuities funded with high quality separate accounts, very much like mutual funds. These contracts, up to that point, had had a stellar track record routinely generation returns of 10-20% annually. They had high management fees but who cares if you are generating double digit returns? Everything was going great, and them BAM! The 2008-09 crash happened. In less than six months, clients lost up to 40% of their account value. It was awful. The standard response to this kind of thing from a broker is always, always “don’t worry it will come back.” More on this below. We don’t want his to happen to you. We want you to make choices that make sense no matter what.

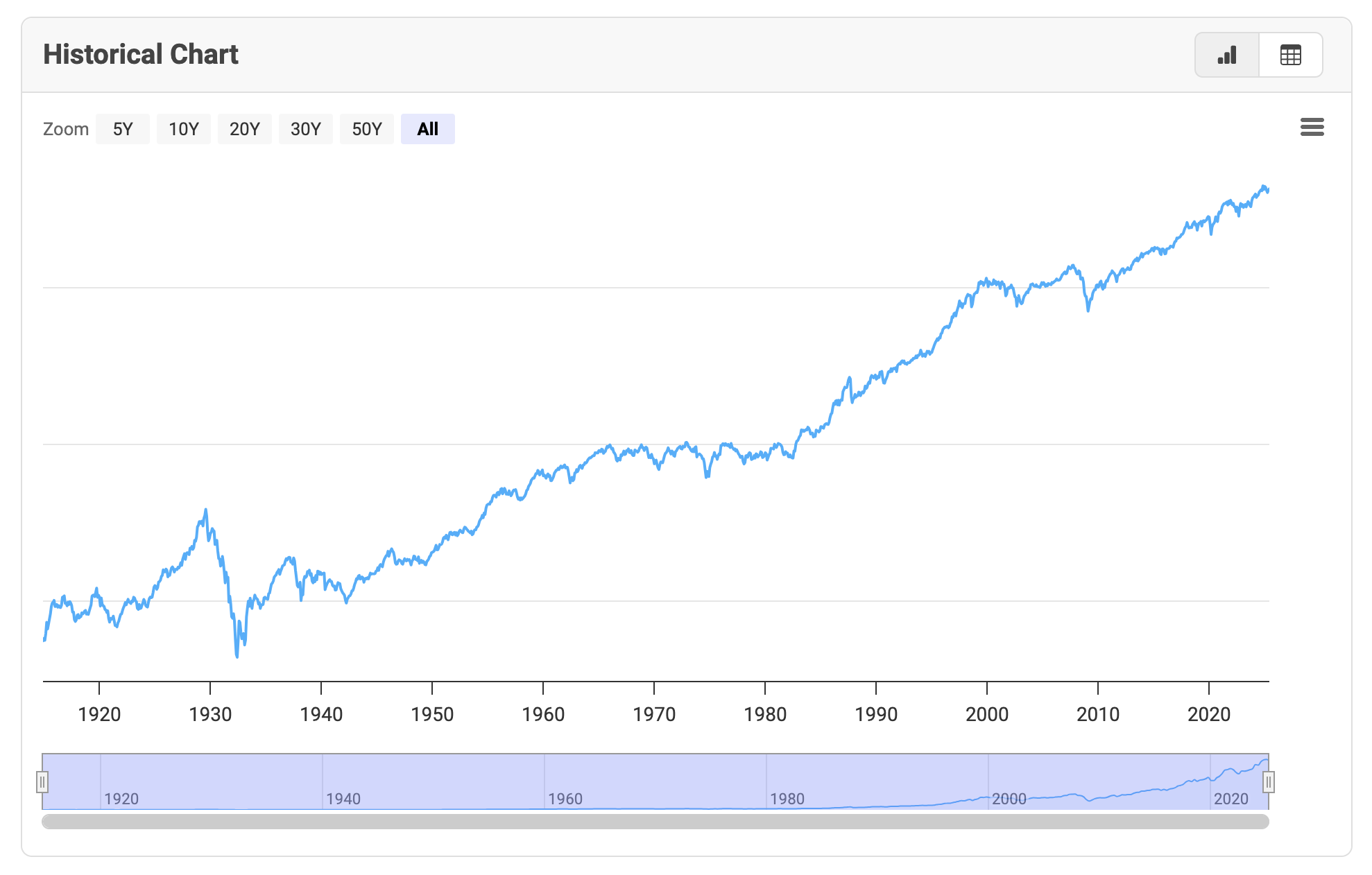

Here are two charts to illustrate this point:

First, a chart showing the Dow since the establishment of the FED.

If you look carefully, you will see the stock market crash of 1929. “But not to worry! It will come back!” Indeed, it did…in late 1954, 25 years.

If you were 65 in 1929, you were probably dead by 1954. So much for your retirement fund. Do not think this can’t happen again. It can. We implore you to learn to prepare for possibilities, not just probabilities.

Next, a chart showing the money supply, what the economists call m1, since 1960.

Note the vertical growth in 2020. Insane, right? That is the basis for the supposedly strong stock market. We believe the current paradigm is unsustainable and that a reckoning is coming because the capital markets can’t be artificially controlled indefinitely. There used to be a margarine commercial with the claim that you could not tell the difference between their product and real butter.

The tag line was quite clever, “It not nice to fool Mother Nature.” I believe there were thunderbolts being hurled by an angry woman, Mother Nature herself. Likewise, it is not nice, indeed dangerous, to fool Mr. Market. He will bring you back to a very harsh reality, eventually. Therefore, this environment is custom made for an Indexed Annuity, and radioactive for Variable Annuities and other equity-based assets.